February 2024 Market Update

Marcus Musson, Forest360 Director

Opinion Piece

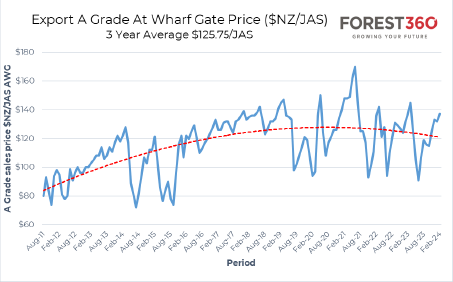

February has kicked off with a hiss and a roar with log exporters pulling out the pencil sharpeners and publishing prices in the mid to high $130’s for A grade (except for Bluff and Lyttleton where you poor folks are between $10 and $20/m3 less). This price level has given forest owners a grin that rivals Chloe Swarbricks’ after James Shaws’ resignation and gives numbers that are at least $10/m3 over both the 3 and 5 year averages. This lift is courtesy of an increased CFR price, lower foreign exchange, and steady shipping rates. It’s not all beer and skittles though and anyone that reads the news will be well aware of the continued issues with the Chinese economy and the embattled construction sector.

The Chinese Evergrande debacle continues to unfold with an order from a Hong Kong court to liquidate the company which currently holds the crown of the worlds most indebted developer with over $300 billion yuan in total liabilities. An attempt by Fengtao Property Company, one of Evergrande’s offshoots, to auction off some of its assets was met with zero bids, which indicates the level of demand in the property sector.

There are some glimmers of light through the dark CCP clouds as Reuters reported that the average Chinese city house price rose 0.15% in January, not really a ‘wow moment’ but it is the fastest gain since mid-2021 with growth occurring in half of the surveyed cities. It was also noted that government land sale revenue also gained 1.8% from the previous year which is the first-time sales have risen in two years. How this is happening when there’s 10 years’ housing supply still in the system is anyone’s guess, but sentiment is a huge driver of the Chinese economy which doesn’t really conform to economics 101.

The China market is even more important to NZ now as a number of sawmills in South Korea have closed their doors. While South Korea isn’t a massive player in terms of volume, it is especially significant in that South Korea accepts non-fumigated cargo from NZ. Most of the NZ log cargo is shipped on vessels that have approximately a third of the cargo ‘on deck’ and therefore this cargo must be fumigated on port prior to loading if going to China. The ‘under deck’ cargo in the holds is fumigated enroute which is reasonably straight forward but following the NZ EPA’s effective banning of Methyl Bromide as a fumigant (by requiring large buffer zones), on deck cargos that cannot be fumigated are now mostly de-barked if destined for China. Delivering top deck cargos to South Korea is a good option for those exporters from ports that don’t have de-barkers or the ability to fumigate, and therefore any reduction in Korean demand also reduces the optionality for NZ exporters.

Chinese log inventories have crept up around 50Km3 in the past month and now sit at around 2.6Mm3 which is approximately 40 days’ supply. Chinese New Year celebrations kick off next week and many sawmills have shut early which explains the inventory build and it’s likely that we will see total inventory at the mid 3Mm3 level by the time everyone returns to work. Total log imports into China for 2024 will likely be similar to 2023 at a shade under 40Mm3 which is around 60% of the 2021 levels. NZ has increased its share and currently accounts for around 45% of this total, which is an increase in terms of market share but a decrease in total volume. Supply from Europe and the US has reduced significantly with the Red Sea scuffle potentially keeping the lid on this for the mean time. Australia has recommenced log exports to China, however only in smaller volumes (once bitten twice shy) with the majority of their export volume destined for India.

Carbon prices have rallied somewhat with current spot prices at $73.35/NZU. This equates to around $2,200/ha/yr and will likely have many sheep farmers looking at trees as a form of succession planning, despite the negative press from the noisy few. The next Govt NZU auction is scheduled for March, and it will be interesting to see if any bids clear the floor price following the failures of 2023. Nicola Willis will be watching very carefully as the auction revenue will probably be factored into the 2024 books to help fill the Roberston fiscal hole.

So, all in all 2024 is shaping up pretty well with solid export prices, strong domestic demand, (especially pruned logs) and a reasonable general outlook. All eyes will be on China demand once everyone returns from new year celebrations and hopefully a few weeks R&R will have them return to work with renewed fizziness about building things with wood. NZ supply will be interesting over the next few months as weather and prices increase woodlot activity, and the Taupo windthrow salvage starts to wind down. Whether we can hold the price gains through into Q2 is yet to be seen but like any good commodity trader, we’ll take what we can get.