March 2024 Market Update

Marcus Musson, Forest360 Director

Opinion Piece

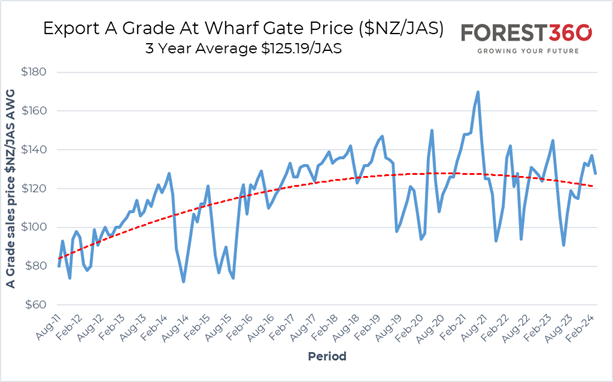

History is a great predictor of the future, and the log market is no different. March export prices have been released and it feels as though we’re trying to climb a barbed wire fence, but the problem is we’re currently stuck with one leg on either side, our crotch is snagged on a barb and our feet are slipping. We’re starting to feel some pain and we’re not sure how much more we’ll have to endure before our feet find firm ground.

March prices have dropped around $10/M3 from February and while a drop was not entirely unexpected, the quantum is a pain point. There’s three key metrics that determine export log prices, CFR price (sales price in $USD in the export market), shipping costs and foreign exchange, and unfortunately all three are causing our feet to slip this month. It’s not unusual for CFR price to drop post Chinese New Year (CNY) holidays as the Chinese populus slowly return to work from the longest break of the year and take a while to crank the various industries back into life. Post holiday demand has been very weak and, with NZ and other countries continuing to supply over the holiday period, inventories have increased around 1Mm3 to around 4Mm3. While historically this figure is at the lower end of the total inventory position scale post CNY, with consistently lower log demand now a new norm, 4Mm3 still represents around 65 days inventory which is similar to previous years’ when demand was significantly higher.

Foreign exchange jumped a cent early in the month following the Reserve Bank Governors’ comments and a generally weaker greenback. Freight has caused our feet to slide the most with the Suez Canal scuffle increasing the bulk vessel demand in the Atlantic and resulting in a shortage of vessels in the Pacific. This has resulted in vessel costs increases of around $US8/m3 over the past 6 weeks and unfortunately, like Adrian Orr, these shipping issues are problematic and likely to be around for a while.

The general outlook for China hasn’t really changed with the property market in its third year of downturn. The country’s leaders have just finished their week-long national congress with pledges to boost employment and stabilize the property market, which has historically made up around a quarter of the economy. However, much like Chloes’ recent post promotion speech, the CCP pledges are long on rhetoric and short on practical and workable solutions. There’s no hiding the demographical issues China is facing with a reducing and aging population which will struggle to fill the availability of new homes currently on the market. The IMF recently released their projections of a 45% fall in housing investment based on 2021 figures and asserted that ‘an accelerated cleanup of distressed developers and other policies will help smooth the path to a smaller, more sustainable role for real estate in the economy’.

There’s no denying the need for a reduction in NZ supply to match the new level of demand in China and this is happening slowly. Volume from our cousins over the ditch has resumed into China, albeit at a low but not insignificant level, and supply from other countries has reduced to a trickle due to a myriad of issues. We have seen a couple of vessel head to India from NZ in recent months, but this isn’t a silver bullet – yet. NZ supply will seasonally start reducing as it gets wet and depending on how far into the undies the barb penetrates, the private sector supply will react accordingly. Longer-term fixed price contracts are becoming an important tool for forest managers to help de-risk the export returns for clients and provide exporters with some committed volume over the medium term with which they can plan sales and shipping rotations.

Carbon continues to trade under $70/NZU with a slight rebound since the government recently announced it has changed its methodology around the calculation of the reserve price for future NZU auctions. Prior to this there had been a decline with a five-month low in early February with commentators noting a selloff likely attributed to an attempt to limit the auction reserve price.

Following the changes to the National Environmental Standards for Commercial Forestry (NESCF) as a result of Gabrielle, new rules round slash management have been legislated with the requirement to remove slash over 2 meters in length and 10cm in diameter on orange and red zoned land (a large chuck of the NZ forest estate). In addition, there cannot be any more than 15m3/ha remaining in the cutover. This has created a fair degree of handwringing amongst councils and forest managers as to how to actually comply with this and how to monitor compliance. The implementation of this legislation nationally, rather than regionally, is a knee jerk reaction to the issues that doesn’t recognize the majority of the woody debris mobilized in cyclone affected regions were actually standing forests that were washed into waterways as the very unstable hillsides failed, rather than slash mobilized from the cutover. It’s going to be a very hard and costly piece of legislation to comply with, especially with the current level of mechanization which is not designed to deal with very small pieces of wood.

So, it looks likely that the next few months may be a bit sticky in terms of prices. Domestic demand will keep the tiller steady, especially for pruned forests, but it may take a while to gain some solid footing on the export front. All going well, we’ll hopefully be able to replace our torn undies later in quarter 2.