Carbon Accounting Categories

In June 2020, the New Zealand government passed legislation aimed to improve the ETS. These improvements included changes to the way that carbon is accounted for within the ETS. The transition period for these changes meant that for a short period, for registrations from 2019 to 2022, there were three models for carbon allocation:

- Sawtooth or Stock change

- Averaging

- Permanent

If you registered before the end of 2022, you had the option of all three. In contrast, from 1 January 2023 you only have the option to enter the averaging and permanent carbon accounting categories.

Sawtooth Carbon Accounting

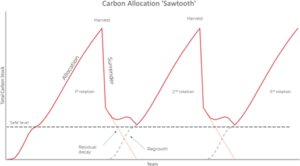

This carbon accounting category for the ETS was only available until 31 December 2022. Under this model, also called ‘stock change’, NZUs are allocated as a forest grows but must be surrendered at the time of harvest.

At the time of harvest, the proportion of NZUs that reflect the above ground biomass of the forest are surrendered and the NZUs that reflect the residual carbon remain. The residual carbon from the first rotation will continue to decay at a constant rate for ten years and is calculated and surrendered over this time. If a second rotation is planted and begins to grow it begins to earn units, balancing out the negative change from the decay, and carbon accrual starts again. Figure 1 shows this occurring over multiple forest rotations.

Figure 1: Multiple rotations of carbon allocation and surrenders under sawtooth carbon accounting.

Averaging Carbon Accounting

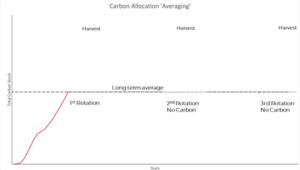

Averaging relates to the average volume of carbon that will be stored in a forest over multiple rotations. This model assumes that as a forest grows and is then harvested, total carbon accumulated fluctuates but there will be an ‘average’ volume that the forest stores.

Under this new category, a forest will be allocated carbon up to the ‘average’ level in the first rotation. No carbon will need to be surrendered when the forest is harvested, as long as the forest is replanted. Although NZUs are not surrendered at harvest if you replant, no further carbon is allocated in subsequent rotations if the forest is grown over the same rotation length e.g., a business-as-usual forestry rotation of 28 years. NZUs are only earned and surrendered using this model if the average age of the forest changes, for example by early or late harvesting. Figure 2 shows carbon allocation up to the long-term average line, with no further carbon allocated from this point.

This method can be applied to ETS-eligible land registered between 2019 and 2022, but from 1 January 2023 this method will be compulsory when registering in the ETS as a new forest unless you enter the ‘permanent’ category.

Figure 2: Carbon allocation under averaging carbon accounting.

Permanent Carbon Accounting

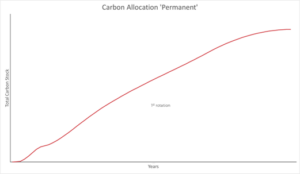

The new permanent carbon accounting category will replace the Permanent Forest Sink Initiative (PFSI) and will be available from 1 January 2023. This category involves the forest owner committing to growing the forest for a minimum of 50 years. This category allows selective harvesting, provided that canopy cover of 30% is maintained.

Carbon allocation for this category uses the sawtooth/stock change accounting method, receiving the full allocation of NZUs as the forest grows. However, if the forest is affected by an adverse event, no surrender liability exists as long as the forest is replanted.

Figure 3: Carbon allocation under permanent carbon accounting.